The rapid growth of digital payments has emerged as a powerful tool for promoting financial inclusion, especially in emerging markets. As millions of people around the world lack access to traditional banking services, digital payment systems are providing them with new opportunities to engage in the global economy. This article delves into the transformative impact of digital payments on financial inclusion, with a focus on how these technologies are closing the gap between banks and unbanked populations. We will explore real-world examples like PayPal, Stripe, and decentralized finance (DeFi) platforms, and examine the challenges and potential of this evolving landscape.

Introduction: The Financial Exclusion Problem

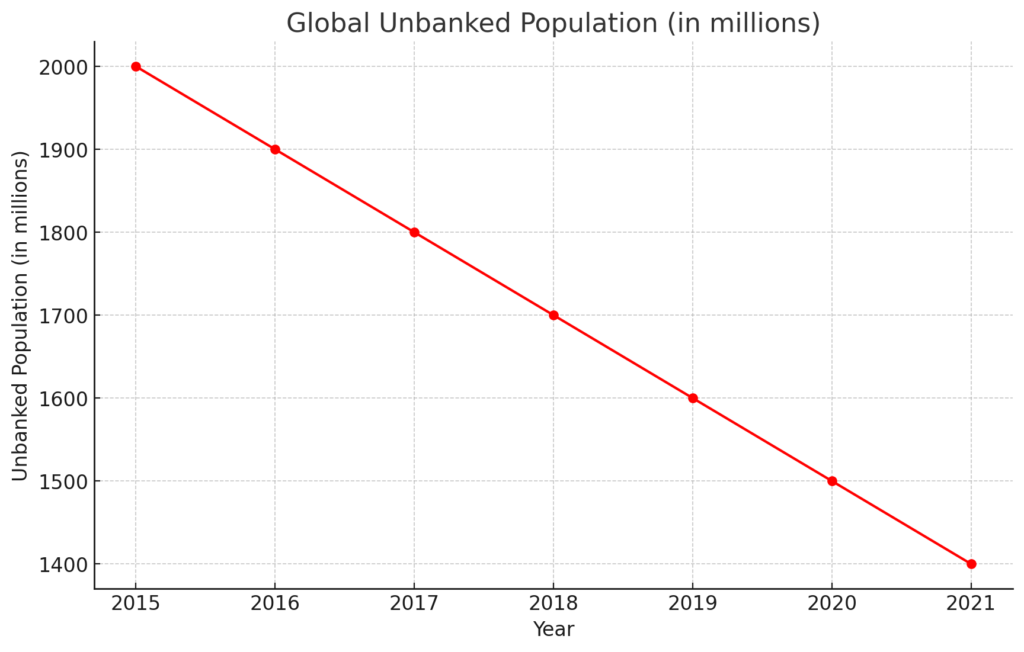

In many parts of the world, traditional banking systems fail to reach significant portions of the population. According to the World Bank, around 1.4 billion adults globally remain unbanked as of 2021. This lack of access to banking services prevents people from saving money securely, obtaining credit, or participating in the formal economy.

The unbanked population is predominantly concentrated in low- and middle-income countries. For these individuals, digital payments offer a lifeline, allowing them to bypass conventional banking institutions and participate in the financial system through their mobile phones or internet-connected devices.

Digital Payments: Redefining Financial Access

Digital payment systems are driving financial inclusion by enabling people to send, receive, and store money without needing a bank account. These systems encompass various forms, including mobile payments, e-wallets, and decentralized finance (DeFi) platforms.

1. Mobile Payment Systems

Mobile payments, where users can send money via mobile phones, have been particularly transformative in sub-Saharan Africa and South Asia. Services like M-Pesa in Kenya have become a vital part of everyday life for millions of people. Initially launched as a mobile money transfer service, M-Pesa has expanded into savings, credit, and insurance, providing financial services to those without access to traditional banks.

According to the GSMA Mobile Economy Report 2022, nearly 1.2 billion people used mobile money services globally in 2021, with sub-Saharan Africa accounting for nearly half of all mobile money transactions worldwide.

2. Digital Wallets and Platforms: PayPal and Stripe

Digital wallets like PayPal, Stripe, and Square have been instrumental in providing financial services to individuals and small businesses. PayPal, with its global reach, allows users to store money, make payments, and send funds internationally. For many individuals in regions without robust banking infrastructure, PayPal offers a secure, accessible alternative to traditional financial institutions.

Stripe, meanwhile, has revolutionized digital payments for small and medium-sized businesses, particularly in regions where access to banking services is limited. By offering a range of payment services—including support for multiple currencies and integration with e-commerce platforms—Stripe enables entrepreneurs to reach global markets without the need for a local bank account.

Decentralized Finance (DeFi): The Next Frontier in Financial Inclusion

While mobile payments and digital wallets have expanded financial access, decentralized finance (DeFi) promises to take financial inclusion to the next level. DeFi refers to a broad category of financial services and applications that operate on blockchain networks, primarily using smart contracts. Unlike traditional financial systems, which rely on centralized entities such as banks or brokers to facilitate transactions and manage assets, DeFi platforms allow users to interact with financial services directly and autonomously. This peer-to-peer nature of DeFi, combined with the transparency and security of blockchain technology, is fundamentally reshaping how people interact with money and financial services.

Key DeFi Innovations

Smart Contracts: Smart contracts are the foundation of DeFi applications. These self-executing contracts are coded to automatically perform transactions when certain conditions are met. For example, a smart contract on a lending platform might automatically disburse a loan once collateral is locked in, without needing an intermediary. The most popular blockchain for building smart contracts is Ethereum, which supports decentralized applications (dApps) and smart contracts. Other blockchains like Binance Smart Chain and Solana have also seen significant DeFi activity.

Decentralized Exchanges (DEXs): Decentralized exchanges allow users to trade cryptocurrencies directly with one another without the need for a central authority. Examples of popular DEXs include Uniswap and SushiSwap. These platforms use liquidity pools, where users can provide funds in exchange for interest or a portion of the trading fees. Unlike traditional exchanges, DEXs are non-custodial, meaning that users maintain control of their funds throughout the trading process.

Lending and Borrowing Platforms: DeFi platforms like Aave and Compound allow users to lend their cryptocurrencies and earn interest or to borrow assets by posting collateral. The lending process is automated through smart contracts, removing the need for financial institutions like banks. Borrowers typically provide over-collateralization to secure loans, ensuring the platform’s solvency.

Stablecoins: Stablecoins are a crucial part of DeFi, providing a more stable form of digital currency that’s tied to real-world assets, like the U.S. dollar or other fiat currencies. These stablecoins, such as USDC or DAI, enable users to engage in DeFi without the extreme price volatility that’s common in cryptocurrencies like Bitcoin or Ethereum.

Yield Farming and Liquidity Mining: Yield farming involves users providing liquidity to DeFi protocols (such as lending platforms or DEXs) in return for rewards, often in the form of tokens. This practice can offer high returns, though it comes with risks, such as price volatility and smart contract vulnerabilities. Liquidity mining is similar, but users receive additional tokens from the protocol in exchange for providing liquidity.

Insurance: Decentralized insurance platforms, such as Nexus Mutual, offer protection against risks like smart contract failure or exchange hacks. These platforms operate similarly to traditional insurance but are managed by decentralized pools of capital instead of insurance companies.

Key Components of DeFi

Smart Contracts:

Smart contracts are the foundation of DeFi applications. These self-executing contracts are coded to automatically perform transactions when certain conditions are met. For example, a smart contract on a lending platform might automatically disburse a loan once collateral is locked in, without needing an intermediary.The most popular blockchain for building smart contracts is Ethereum, which supports decentralized applications (dApps) and smart contracts. Other blockchains like Binance Smart Chain and Solana have also seen significant DeFi activity.

Decentralized Exchanges (DEXs):

Decentralized exchanges allow users to trade cryptocurrencies directly with one another without the need for a central authority. Examples of popular DEXs include Uniswap and SushiSwap. These platforms use liquidity pools, where users can provide funds in exchange for interest or a portion of the trading fees.Unlike traditional exchanges, DEXs are non-custodial, meaning that users maintain control of their funds throughout the trading process.

Lending and Borrowing Platforms:

DeFi platforms like Aave and Compound allow users to lend their cryptocurrencies and earn interest or to borrow assets by posting collateral. The lending process is automated through smart contracts, removing the need for financial institutions like banks. Borrowers typically provide over-collateralization to secure loans, ensuring the platform’s solvency.

Stablecoins:

Stablecoins are a crucial part of DeFi, providing a more stable form of digital currency that’s tied to real-world assets, like the U.S. dollar or other fiat currencies. These stablecoins, such as USDC or DAI, enable users to engage in DeFi without the extreme price volatility that’s common in cryptocurrencies like Bitcoin or Ethereum.

Yield Farming and Liquidity Mining:

Yield farming involves users providing liquidity to DeFi protocols (such as lending platforms or DEXs) in return for rewards, often in the form of tokens. This practice can offer high returns, though it comes with risks, such as price volatility and smart contract vulnerabilities.Liquidity mining is similar, but users receive additional tokens from the protocol in exchange for providing liquidity.

Insurance:

Decentralized insurance platforms, such as Nexus Mutual, offer protection against risks like smart contract failure or exchange hacks. These platforms operate similarly to traditional insurance but are managed by decentralized pools of capital instead of insurance companies.

Advantages of DeFi

Accessibility:

DeFi platforms are open to anyone with an internet connection, enabling financial services to reach people who are unbanked or underbanked, especially in developing regions.

Transparency:

Since DeFi protocols operate on public blockchains, all transactions are transparent and available for anyone to verify. This creates a high level of trust between participants and ensures that the system operates fairly.

Control Over Assets:

Users have full control of their funds when using DeFi platforms. Unlike traditional banking systems, where banks hold custody of your money, DeFi allows users to manage their assets directly through their digital wallets.

Innovation:

DeFi has led to the creation of new financial products and services that are difficult or impossible to achieve in traditional finance, such as flash loans (loans that are borrowed and repaid in a single transaction) and automated market-making (AMM) systems that provide liquidity.

Challenges of DeFi for Financial Inclusion

Despite its potential, DeFi faces significant challenges in promoting financial inclusion. These include:

Volatility and Risk: Cryptocurrencies are inherently volatile, and the value of assets locked in DeFi platforms can fluctuate dramatically. Moreover, because DeFi is relatively new, the space is prone to technical risks, including smart contract bugs and vulnerabilities. Some platforms have also experienced “rug pulls,” where malicious actors siphon away liquidity, leading to significant losses for users.

Regulatory Uncertainty: The regulatory environment surrounding DeFi is still unclear in many parts of the world. While DeFi offers freedom from traditional financial regulations, governments are beginning to focus on how to regulate decentralized platforms, especially when it comes to issues like money laundering or fraud prevention.

Security Concerns: Although blockchain technology is generally secure, DeFi protocols are vulnerable to hacking and exploits. For example, DeFi platforms have been targeted through flash loan attacks, where attackers manipulate asset prices to drain liquidity pools.

Complexity: DeFi platforms can be difficult for beginners to understand and use. Engaging in DeFi requires knowledge of digital wallets, understanding how smart contracts work, and being aware of potential risks. This learning curve can deter mainstream adoption.

The Future of DeFi

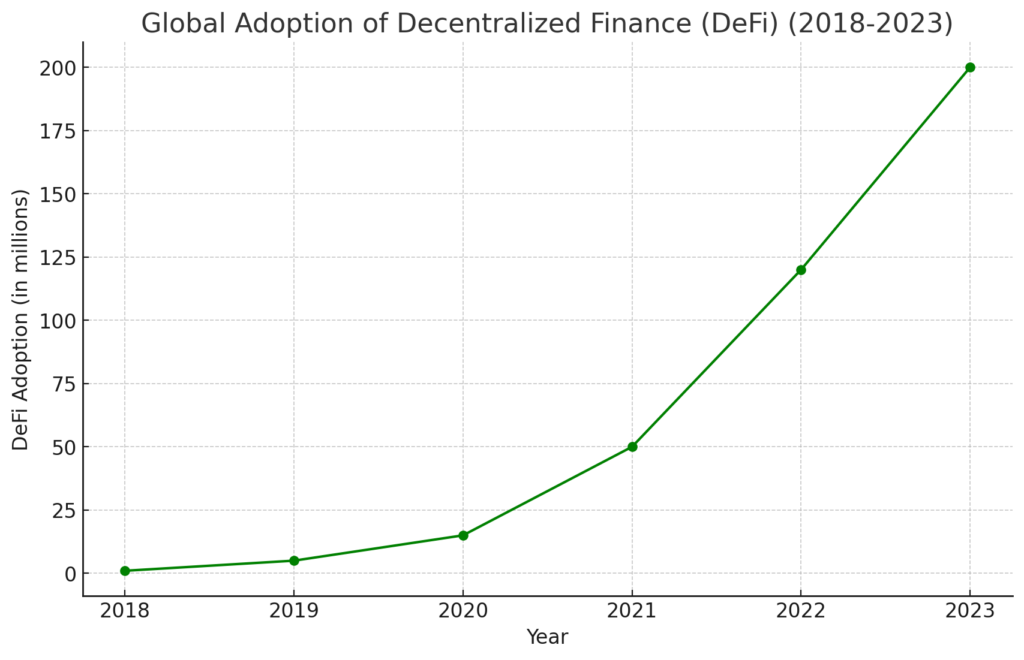

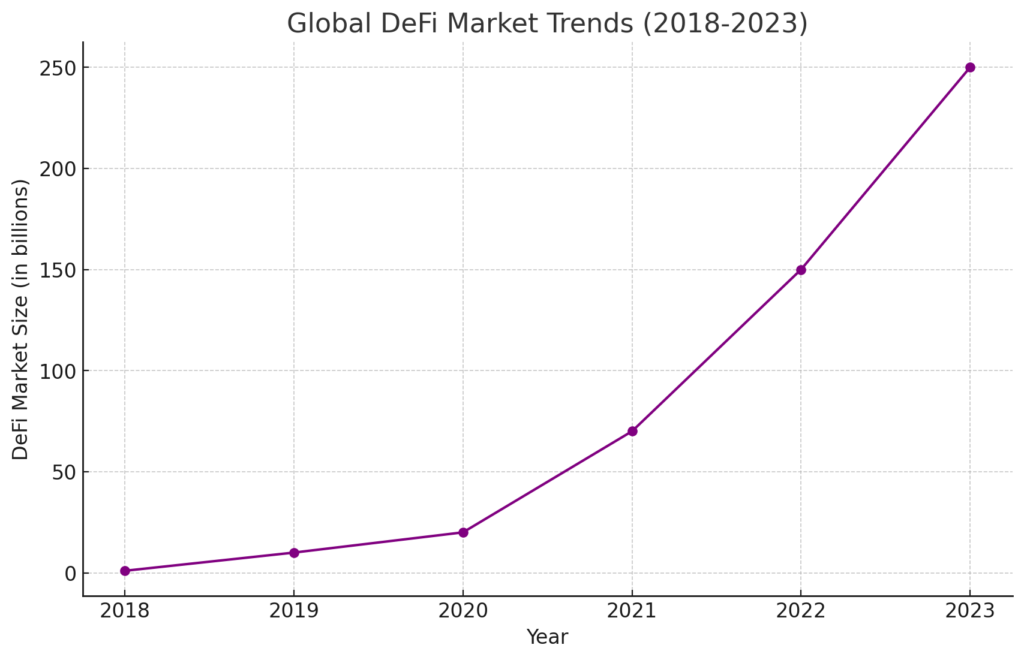

The DeFi sector is expanding rapidly, with the total value locked (TVL) in DeFi protocols exceeding $200 billion in 2023. As the space matures, we can expect greater innovation and more user-friendly platforms, which could bring DeFi into the mainstream. Several trends and developments point toward a promising future for DeFi:

Interoperability:

As more blockchain networks support DeFi applications, interoperability between different blockchains will become essential. Projects like Polkadot and Cosmos are already working on creating networks that connect various blockchains, allowing DeFi protocols to operate seamlessly across multiple platforms.

Institutional Adoption:

While DeFi was initially a space for crypto enthusiasts, it is starting to attract institutional players, such as hedge funds and asset managers, who are drawn to its high yields and innovative financial products. As institutional involvement increases, it could bring more liquidity and legitimacy to the DeFi space.

Integration with Traditional Finance:

We are beginning to see the merging of traditional finance (TradFi) with decentralized finance (DeFi), with some banks exploring ways to use blockchain technology for services like lending and cross-border payments. This integration could further bridge the gap between the traditional financial system and the decentralized world.

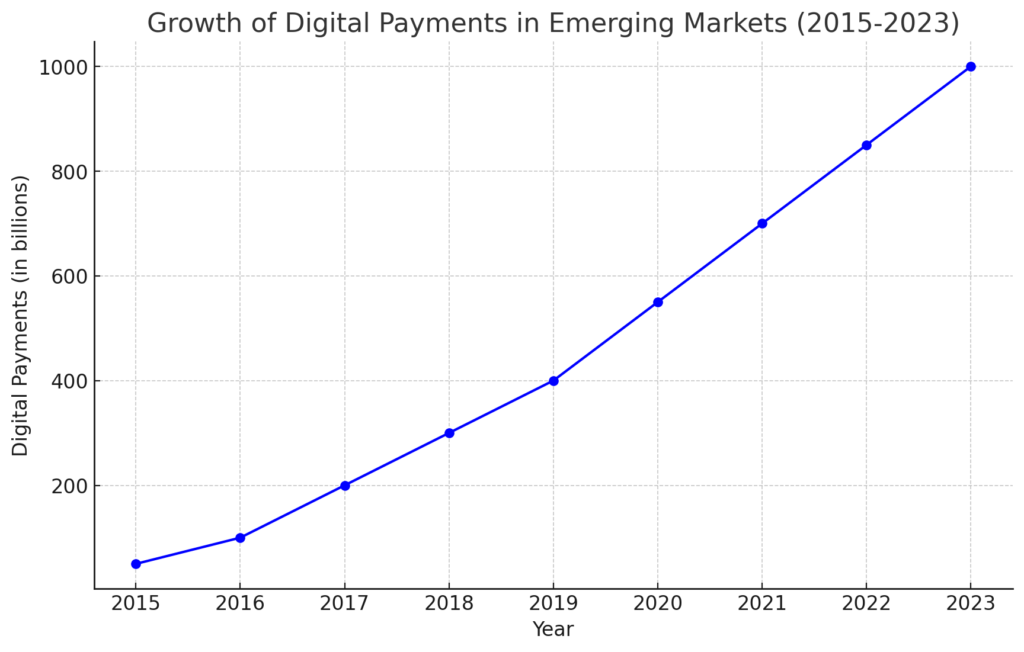

The Impact of Digital Payments on Emerging Markets

Digital payments are having a profound impact on emerging markets, where large segments of the population are unbanked or underbanked. By lowering the barriers to financial services, digital payments are enabling economic growth, fostering entrepreneurship, and empowering individuals to improve their financial well-being.

1. Empowering Small Businesses

In many emerging markets, small and micro-enterprises are the backbone of the economy. However, these businesses often face significant challenges when it comes to accessing credit and making or receiving payments. Digital payment platforms like PayPal and Stripe are helping small businesses overcome these obstacles by providing them with the tools they need to conduct business online, accept payments from customers, and manage their finances more effectively.

For instance, Stripe’s Atlas program allows entrepreneurs in developing countries to incorporate a U.S.-based company and open a U.S. bank account, giving them access to international markets and financial services that would otherwise be out of reach.

2. Boosting Remittances and Cross-Border Payments

Remittances are a vital source of income for millions of families in emerging markets. However, traditional remittance services like Western Union are often expensive and slow, with fees that can exceed 10% of the transaction amount. Digital payment systems, including blockchain-based platforms like Ripple and Stellar, are significantly reducing these costs and enabling faster transactions.

The World Bank estimates that reducing remittance fees to below 5% could save families in low-income countries up to $16 billion annually. Digital payments, with their lower fees and faster processing times, are making this a reality for millions of people.

Challenges and Opportunities for Widespread Adoption

While digital payments hold enormous potential for promoting financial inclusion, several challenges remain. These include:

- Infrastructure: In many developing countries, access to the internet and reliable mobile networks remains limited, hindering the adoption of digital payments.

- Digital Literacy: Many unbanked individuals lack the technical skills needed to use digital payment platforms effectively. Educating these populations will be crucial for driving adoption.

- Trust: In regions where financial scams and fraud are prevalent, gaining the trust of the unbanked will be essential for the success of digital payment initiatives.

Despite these challenges, the opportunities for growth are immense. The International Monetary Fund (IMF) has noted that expanding access to digital financial services could increase GDP growth rates by 1% in emerging markets, demonstrating the potential of these technologies to drive economic development.

Conclusion: A More Inclusive Financial Future

Digital payments are playing a crucial role in closing the financial inclusion gap, particularly in emerging markets. By providing individuals and small businesses with access to affordable, secure, and convenient financial services, digital payment platforms are empowering millions of people to participate in the global economy.

As innovations like decentralized finance (DeFi) continue to evolve, the potential for further financial inclusion is enormous. However, realizing this potential will require overcoming significant challenges, including infrastructure limitations, regulatory uncertainty, and the need for digital literacy.

With the right investments in technology and education, the future of digital payments looks bright, and the dream of universal financial inclusion may soon become a reality.

Sources:

- World Bank. (2021). Global Findex Database: Measuring Financial Inclusion.

- GSMA Mobile Economy Report 2022. Global Mobile Financial Services.

- IMF (2023). The Role of Digital Finance in Emerging Markets.

- PwC. (2023). The Future of Financial Services: Embracing Digital Disruption.

- World Bank. (2022). The Global Cost of Remittance: A Closer Look.